© The Wharton School, The University of Pennsylvania | Wharton Global Youth Program | Resources for Educators: Lesson Plans 1/7

Compound Interest

SUBMITTED BY: Nina Hoe, University of Pennsylvania

SUBJECT(S): Computation

GRADE LEVEL(S): 9, 10, 11, 12

☰ OVERVIEW:

This lesson begins with a brief whole class discussion of different types of interest. In small

groups, students will compare simple interest and compound interest through computations.

Students will explore more deeply the function and implications of compound interest and

graphically represent their findings. The lesson closes with a whole class discussion about

compound interest and when/where it is used.

☰ RELATED ARTICLES:

“Your Money: 3 Questions for CNote’s Yuliya Tarasava”

“Why It Pays to Save: Knowing the Time Value of Money”

“The Rising Costs of a U.S. College Education”

“The Power of Plastic: What to Know about What You Owe”

“The Ins and Outs of Interest — from a Student Loan Survivor”

“Student Essay: Saving for Retirement: ‘Time Is on Our Side’”

“Payday Loans and the Perils of Borrowing Fast Cash”

“Olivia Mitchell on Why Young Consumers Should Just Say No to Spending”

“British Couponer Extraordinaire: Jordon Cox Is a Savings Sensation”

“A Trip to the Bank, Lollipops and World Savings Day”

“9 Insights About Negative Interest Rates”

Standards:

© The Wharton School, The University of Pennsylvania | Wharton Global Youth Program | Resources for Educators: Lesson Plans 2/7

WGYP:

Mathematical Foundations

Number Relationships

Patterns, Functions, and Algebra

Problem Solving

Common Core:

A-SSE.1.Interpret expressions that represent a quantity in terms of its context

A-CED.1.Create equations and inequalities in one variable and use them to solve problems.

Include equations arising from linear and quadratic functions, and simple rational and exponential

functions.

A-CED.2.Create equations in two or more variables to represent relationships between

quantities; graph equations on coordinate axes with labels and scales.

F-IF.1. Understand that a function from one set (called the domain) to another set (called the

range) assigns to each element of the domain exactly one element of the range. If f is a function

and x is an element of its domain, then f(x) denotes the output of f corresponding to the input x.

The graph of f is the graph of the equation y = f(x).

F-IF.2. Use function notation, evaluate functions for inputs in their domains, and interpret

statements that use function notation in terms of a context.

Objectives/Purposes: Students will understand and be able to compute compound interest and

graphically represent the outcomes. They will be able to distinguish between compound and

simple interest.

Other Resources/Materials:

Calculators

Class Discussion:

Simple Interest

I = P ∙ r ∙ t

© The Wharton School, The University of Pennsylvania | Wharton Global Youth Program | Resources for Educators: Lesson Plans 3/7

Where I is the interest earned or owed in dollars, P is the principal amount deposited, lent, or

borrowed, r is the interest rate (the percent) in decimal form, and t is the time in years that the

money is in the account, lent, or that the borrower takes to pay back the loan.

There are different types of interest. In the last lesson, we calculated simple interest rates.

1. Are there other types of interest other than simple interest?

2. How do other types of interests work?

3. Who determines interest rates?

Have students work in small groups or pairs.

(Have 2 two groups of students do the computations for Case 1 and 2 on the board side-

by-side Have another 2 groups of students be responsible for columns 3 and 4 – questions

7 and 8.)

Activity:

Student Worksheet

Simple vs. Compound

Case 1:

1. You invest $1,000 in savings account that earns 3% interest for 3 years.

1. Find the amount of simple interest that you would earn at the end of a 3-year

period. [use P = Irt] ($90)

2. What is the total amount of money that you will have after this 3-year period?

($1,090)

Case 2:

1. You invest $1,000 in savings account that earns 3% interest for 1 year.

1. Find the amount of simple interest that you would earn at the end of a 1-year

period. [use P = Irt] ($30)

2. What is the total amount of money that you will have after this 1-year period

($1,030)

© The Wharton School, The University of Pennsylvania | Wharton Global Youth Program | Resources for Educators: Lesson Plans 4/7

2. Take the total amount of money that you have from #2 part b and put it back into the

same account for another year.

1. Find the amount of simple interest that you would earn at the end of a 1-year

period. [use P = Irt] ($31.83)

2. What is the total amount of money that you will have after this 1-year period?

($1,060.90)

3. Take the total amount of money that you have from #3 part b and put it back into the

same account for another year.

1. Find the amount of simple interest that you would earn at the end of a 1-year

period. [use P = Irt] ($30.93)

2. What is the total amount of money that you will have after this 1-year period?

($1,092.73)

4. How does the total amount of money that you have after 3 years from Case 1 compare

to the total amount of money you have from Case 2? ($1,090 vs. $1,092.73 = $2.73

more. Imagine how much larger this could be over a longer period of time and with

even more money.)

In Case 2, the interest was compounded, meaning that the interest is earned not only on the

principal but on the interest that was previously earned as well.

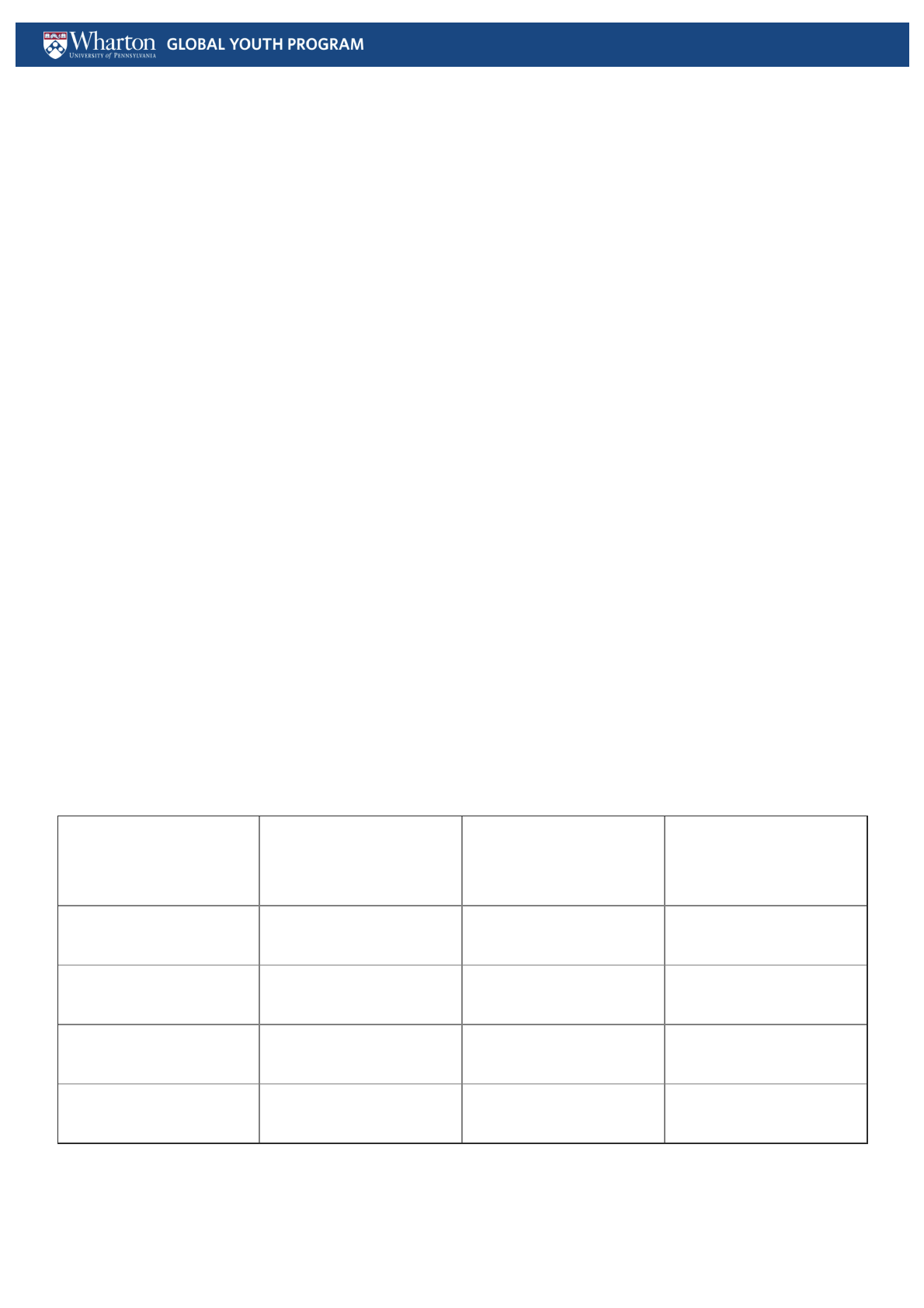

1. Complete the following table showing the balance of your account using compound

interest. (The 3 and 4 columns will be blank for right now.)

Time (years) Balance (dollars) Balance in terms of

previous balance

Balance in terms of

original balance

0 $1,000 100% 100%

1 $1,030 103% 103%

2 $1,060.90 103% 106%

3 $1,092.73 103% 109%

1. For successive years, what percent of the previous balance is the new balance?

1. Years 0 to 1: _________

rd th

© The Wharton School, The University of Pennsylvania | Wharton Global Youth Program | Resources for Educators: Lesson Plans 5/7

2. Years 1 to 2: _________

3. Years 2 to 3: _________

4. What do you notice about the percentages?

5. Write each balance in terms of the previous balance (record in column 3).

2. Write each balance in terms of the original balance (record in column 4).

The general form for compound interest (an exponential growth model) is the equation:

where, P is the principal amount, or the original amount of money before any growth occurs, r is

the annual nominal interest rate or the growth rate in decimal form, n is the number of times the

interest is compounded per year, t is the number of years, and A is the new amount.

Formula for Interest Compounded Annually:

Formula for Interest Compounded Half Yearly:

Formula for Interest Compounded Quarterly:

1. What is the growth rate from Case 2? (9%)

2. You invest $650 into a savings account that earns 2.5% interest, compounded yearly.

Write a model for the account balance y after t years.

[A = $650(1 + .025)^t

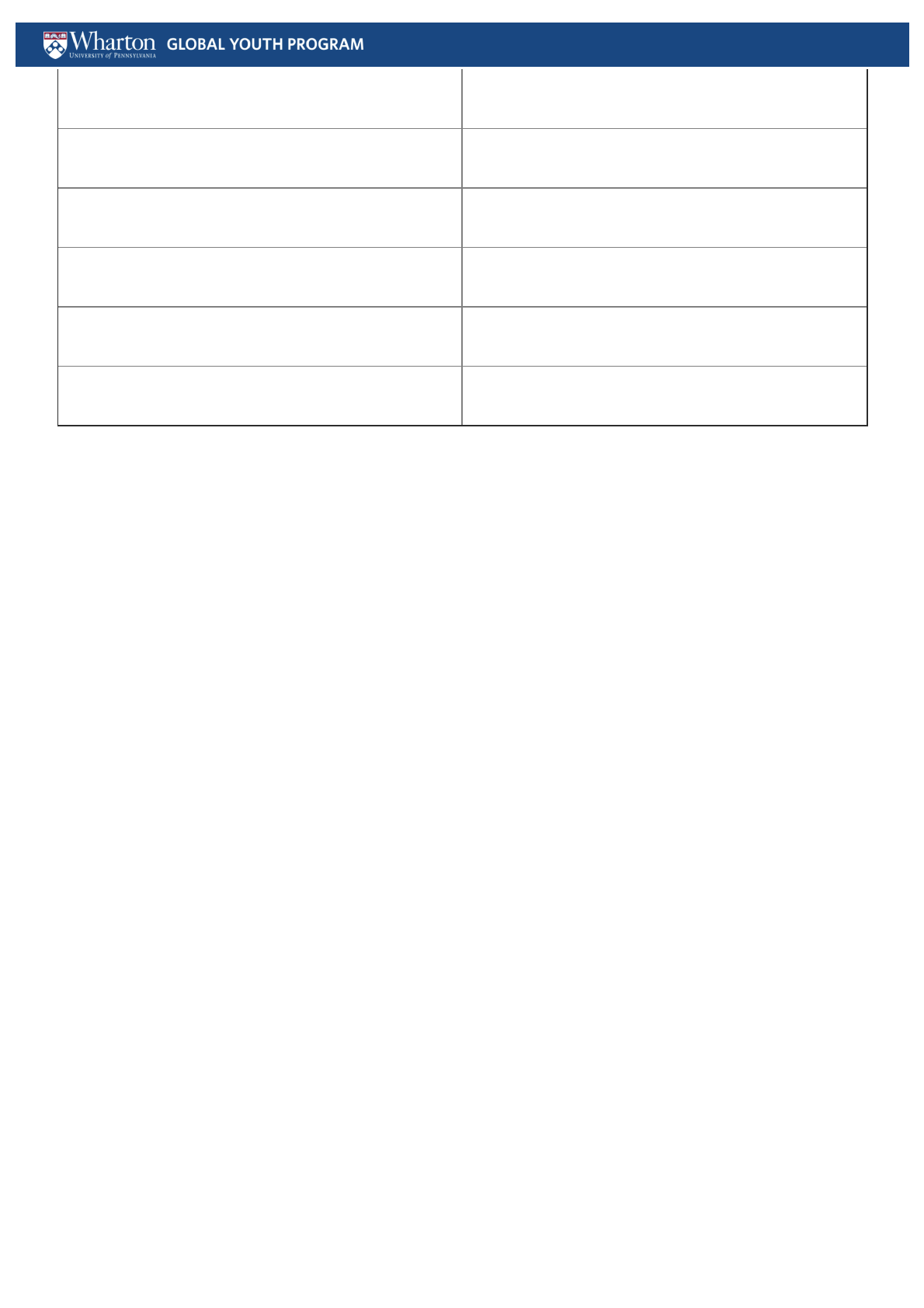

1. Complete the following table of values showing the account balance as a function of

time (years the money is in the account).

Time (years) Account Balance (dollars)

© The Wharton School, The University of Pennsylvania | Wharton Global Youth Program | Resources for Educators: Lesson Plans 6/7

0 $650

1 $666.25

2 $682.91

5 $735.42

10 $832.05

15 $941.39

1. In the space below, create a graph that shows the account balance as a function of the

time.

[Before you graph, make sure to identify:

Variable quantity:

Lower Bound:

Upper Bound:

Interval: ]

1. Use the graph to determine how long you have to keep the account open in order to

have

1. a balance of $700. (3 years)

2. a balance of $800. (between 8 and 9 years)

2. You have $1,000 that you want to invest for 5 years before you use the money towards a

large purchase. Your bank offers a simple interest rate of 3% or an annual compound

interest rate of 2.7%. Assuming that you will leave the money in 5 years, what is the best

way to invest with your bank? (Simple – $150 in interest, Compound – $142.49)

3. Based on the previous questions, do you think compounding interest annually, half

yearly, or quarterly will yield more or less money? (The more it’s compounded, the

faster it grows)

© The Wharton School, The University of Pennsylvania | Wharton Global Youth Program | Resources for Educators: Lesson Plans 7/7

4. Calculate the annual, half yearly, and quarterly compounded interest associated with

investing $5,000 for 4 years at an interest rate of 2.5%

1. Annually ($5,125)

2. Half Yearly ($5,125.78)

3. Quarterly ($5,126.18)

Tying It All Together:

Whole class discussion:

{kind=link}

{kind=link}

{kind=link}

{kind=link}